Introduction

If a lay person knows who Hyman Minsky is, it is likely that they associate him with a sagacity about debt and its role in the Global Financial Crisis. And their conception of debt, more or less, would likely be that humans have an insatiable appetite for debt that eventually cannot be paid back, and, once the public has become aware of the gap between income streams and financial obligations, the economy begins to crumble. The suspicion is that debt is inherently destabilizing.

That person’s belief is accurate with respect to private sector debt. Economic expansion fuels optimism, which encourages risk-taking in the form of debt, which fuels more expansion— until, eventually, the debts cannot be paid back because the economic reality does not meet past expectations. Then the defaults begin, businesses close, unemployment rises, and families lose their livelihoods. The contraction of debt makes recessions more brutal, too. During both contractions and expansions, then, private sector debt acts pro-cyclically.

In my view, Minsky’s proposal that Central Banks raise rates to prevent unsustainable expansions and Governments launch massive fiscal stimulus to combat downturns are pointless to elaborate on. That theory is already part of mainstream policy making; a few sentences about the topic is already too much. More importantly, given that we have unlocked the door towards a world of fiscal dominance via massive government deficits, the actually meaningful question becomes what should the government spend money on?, which, in Minsky’s view, is the elimination of involuntary employment. This proposal would not only combat unemployment and income inequality, but the fact that such a project would rely on massive amounts of public debt would decrease aggregate private debt and therefore stabilize the economy.

Private Debt is Destabilizing

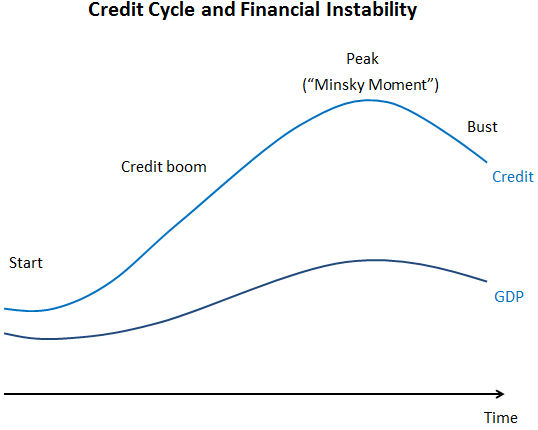

The quick and dirty way to instill an appreciation for finance is to address fundamentals about businesses. Starting a business requires investments in capital and labor: two essential components of any enterprise. These investments, in the absence of a rich uncle, require financing, which is to say that the entrepreneur must take-on debt. All economies rely on investment spending and all investment spending relies on financing. This vital synergy between private debt and growth creates instability in economies and societies at large.

In good times, this system works very well. Businesses earn profit margins that are large enough to pay-off interest payments and the principal on the loan. Minsky calls this “hedge financing,” but the technical term doesn’t matter. A bank lent money that enabled a productive enterprise to provide desirable goods or services to the public and create employment opportunities for citizens. It’s good vibrations and what we all hope for.

Expansionary economic environments encourage more risk-taking. A growing economy stirs bullish animal spirits, makes creditors and debtors more optimistic about the future, and causes lenders and borrowers to incur more debt as they expect growing profit margins. Increased investment means more jobs, too, which sustains aggregate demand. Economic reality reinforces risky behavior— not problematic human psychology.

Eventually, during an expansion, it is common to witness “speculative financing,” which is when revenues are robust enough to pay off interest payments but not the principal. This requires short-term debt to be rolled over when it becomes due, and forty years of decreasing interest rates has encouraged this style of financing because low rates ensure that this can be done in a cost effective manner. Businesses have less cushion against disappointments under this regime, but expectations are strong enough to encourage it.

But eventually economic fundamentals do not support the massive amounts of private debt. Profit margins become less robust than anticipated and households do not receive the wage/salary they thought they would. Some may try to engage in “ponzi finance,” which is borrowing to pay interest payments, but, eventually, creditors appraise the situation. Defaults begin, businesses close, homes get foreclosed, unemployment rises, and families lose their livelihoods. Aggregate demand decreases, which allows for the loop to repeat itself.

It is simple to see how the optimism associated with economic expansions sows the seeds of destruction and causes the next recession. None of this requires that we view bankers as evil or borrowers as stupid. Economic reality affirmed their optimism all the way through.

The Economy Lacks Jobs, Not Well-Trained Citizens

In Minsky’s eyes, it becomes essential to limit the instability of the economy. This requires that the government provide massive fiscal stimulus during recessions and the Fed raise rates when the economy risks overheating. This cuts off the left tail of depressive ruts and the right tail of rapid, unsustainable growth.

In that sense, Minsky has already largely been digested and packaged into mainstream discourse. When aggregate demand collapsed in March 2020, the United States Congress provided so much stimulus that national income increased during the recession. Now, two years later, the common consensus — in financial media, Eurodollar futures, and the Fed’s Dot Plot — is that the Federal Reserve should raise rates multiple times this year in order to slow the economy down to tame inflation. The two most recent years reveal that re-reading Minsky does not offer much on that front.

But the current conversation does overlook how Hyman Minsky differed from the mid-20th century legacy left behind by John Maynard Keynes, whose theories had become fully actualized in America during Lyndon B. Johnson’s War on Poverty program. That program aimed to transfer funds (i.e. welfare) and provide education in order to lift people out of poverty. This, in theory, would make people more ready to enter the private sector workforce. But in Minsky’s view, unemployment stems from a lack of jobs — not a personal deficit that unemployed people have. The problem is the economy, not the poor. And the solution is for the government to provide jobs.

The most radical aspect of Minksy’s macroeconomic policy is that the government should become Employers of Last Resort. Local governments would establish what kinds of work would be vital to the community and then provide jobs doing that work to anybody who showed up. This wage would set a minimum wage, allow people to learn good habits and skills necessary to advance in the workforce, and increase the productivity of the population towards common goods (e.g. maintaining public grounds, assisting with COVID testing, manufacturing PPE, etc.). Private sector actors would be free to recruit from these workplaces, too. It would provide income greater than that offered by welfare programs, too, thereby decreasing the lower class’ reliance on debt— which would also stabilize the economy. Although the relevance of this point is disputable, Minsky also adds that this measure, unlike money transfers, is not inflationary since it also raises productivity.

There is always some segment of the population that will want to work but cannot find a job, and this number is absolutely higher than reported unemployment rates because discouraged workers do not count towards those statistics. That segment of the population should not have to suffer the economic and psychological damage that stems from the private sector’s refusal to work for them. In light of the opioid epidemic in the United States, providing employment is also an imperative for our citizens’ well-being. The government can and must provide jobs for those that the private sector refuses to employ.

By contrast, Keynesian prime pumping — which tries to provoke private sector investment through tax cuts, low interest rates, small stimulus, etc. — exacerbates inequality and instability. Such policies favor workers who already have jobs and people who are owners of capital. After decades of this macroeconomic approach, many lower-income families cannot distinguish a recession from a recovery because wages never rise and economic precarity remains persistent. The pump priming relies on an expectation that the private sector lead economic growth, which has yet to be seen, and, even if it were successful, it would require massive amounts of private debt, which we know is destabilizing.

A jobs creation program, on the other hand, would address income inequality since its beneficiaries are those who earn the lowest wages— or no wages at all. It improves social mobility by providing on-the-job training, which would make them more appealing to other employers if the worker wanted to move on from the program. The method of public financing prevents unsustainable booms. And judging by the success of the FDR administration, who devised several jobs creation programs, such measures would be immensely popular.

Transfer of Debt

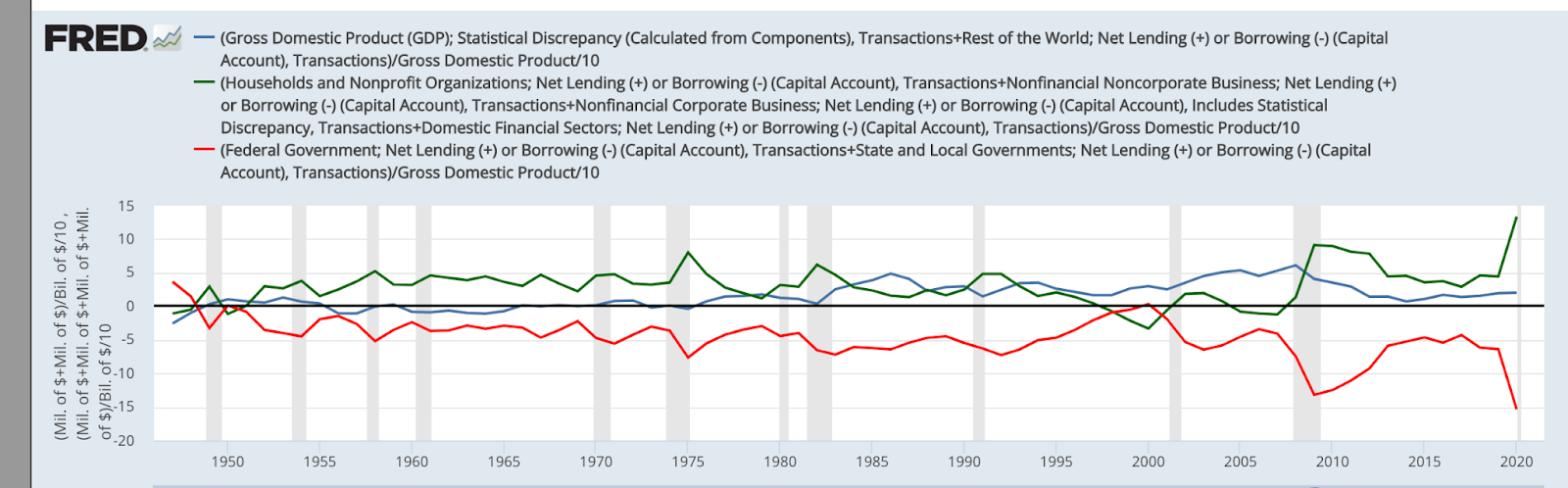

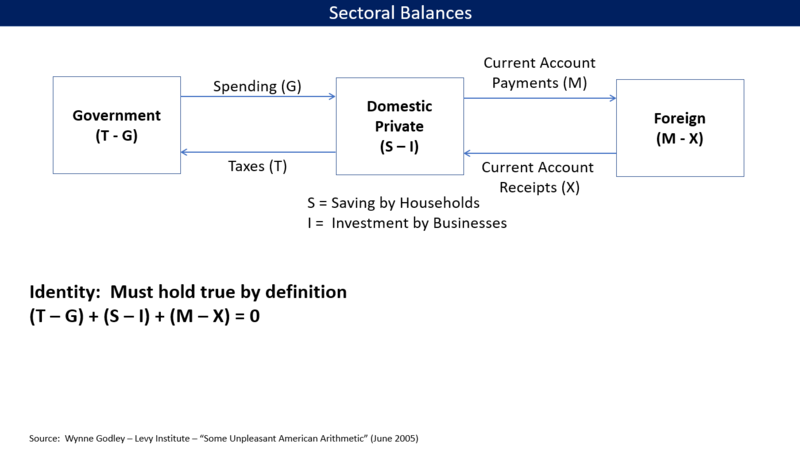

One way to conceptualize Minsky’s move is to think of it as a shift away from private debt to public debt in financing the economy’s growth. The cleanest way to think of this is the “three balances” approach devised by Wynne Godley at the Levy Institute: the balances of the private sector, the government sector, and foreign sector must be zero.

First, if the government runs a surplus, that means it is taking more money than it is giving, which requires that the private sector run a deficit with respect to the government; the opposite is true: if the government runs a deficit, then the private economy is in a surplus. We then add in foreign accounts to represent the United States in its totality. Initially, I was suspicious of this, but the historical data makes this claim very compelling:

The mathematically inclined may prefer to look at this way:

Therefore, government deficits, which must be accepted in order to run a Minsky-style jobs program, must be accepted not as necessary evils, but, instead, as productive necessities. Government deficits help prevent the private sector from accruing too much debt; during a government surplus, the government takes more than it receives. The multicolored graph shows that while the Clinton Administration was running government surpluses, the private sector was forced to decrease its surpluses until the end of the 1990s, when the private sector was spending roughly 106% of the money that it earned. Such a scenario forces the economy to rely on the dynamics that Minsky showed creates financial instability; such a system cannot help but be the engine of its own ruin. In that light, it is no surprise that a recession followed the Clinton administration and that the pre-GFC witnessed the shrinking government deficits and growing household deficits. By 2008, household debt had reached over 100% of GDP.

Unlike the private sector, The Government has unlimited firepower because Minsky’s credit cycle does not apply to the US Government because it has zero credit risk. A government can always pay back debts denominated in the currency that it issues. The money printing this requires may be inflationary — Japan is a case study in which government spending rises and deflation persists — but it can always be done. Despite the current hysteria about government spending and inflation, the 10 Year US Treasury yield closed 2021 at 1.52%, which is far from concern about embedded inflation.

Private debt, not public sector debt, is what destabilizes economies and over reliance on private debt can be avoided with larger fiscal deficits. Public debt is what allows private citizens to live within their means.

Conclusion

Economics cannot be reduced to a hard science. Policy proposals always come prepackaged with the seeds of an ideology that declares what kind of world we should live in. While Minsky’s analysis about private and public debts and economic stability is correct, the topic of jobs deserves a harder look.

After all, David Graeber’s book, Bullshit Jobs, highlights the fact that tens of millions of Americans feel that their jobs are entirely pointless. Not only do they not serve an economic function, but the jobs are soul-sucking. In that light, it seems fair to ask if we might want an economy with fewer jobs that replaces wages/salaries with a Universal Basic Income.

My answer to that would be that both can coexist. A job guarantee does not preclude a UBI scheme. Undoubtedly, there will be a segment of the population that cannot work: the elderly, the disabled, and the young; such groups should not be asked to work, and, therefore, a just society would provide for them. On the other hand, however, there will be a segment of the population that will want to work despite being unemployed— and those people should not be forced to languish without jobs, especially in light of the tight correlation that exists between unemployment and opioid overdoses in the United States. We can and must provide jobs for those that the private sector refuses to employ.

A new question then arises: what kind of jobs should the government provide? Any answer will be pure ideology, for it is the same as asking what society should be like, but, to me, we cannot leave out the crises emerging in the following fields: ecology, education, housing, infrastructure, and healthcare. By devising a jobs creation program, the United States could mobilize the people and not just money to resolve these thorny issues.

Further Reading

Graeber, D., & Roy Élise. (2019). Bullshit jobs. Éditions les Liens qui libèrent.

Kelton, S. (2021). The deficit myth: Modern monetary theory and the birth of the people’s economy. PublicAffairs, Hatchette Book Group.

Wray, L. R. (2017). Why Minsky Matters: An Introduction to the Work of a Maverick Economist. Princeton University Press.

Links to Relevant Data

- Sectoral Balances: https://fred.stlouisfed.org/graph/?graph_id=794489

- Sectoral Balances: https://en.wikipedia.org/wiki/Sectoral_balances

- Household Deposits: https://fred.stlouisfed.org/series/BOGZ1FL193020005Q

- Real Disposable Personal Income: https://fred.stlouisfed.org/series/DSPIC96

- Household Debt to GDP: https://fred.stlouisfed.org/series/HDTGPDUSQ163N

- Employment and Opioid ODs: https://www.usnews.com/news/articles/2017-02-27/opioid-deaths-rise-with-unemployment-report-says

- Ten Year Treasury Yield: https://fred.stlouisfed.org/series/DGS10